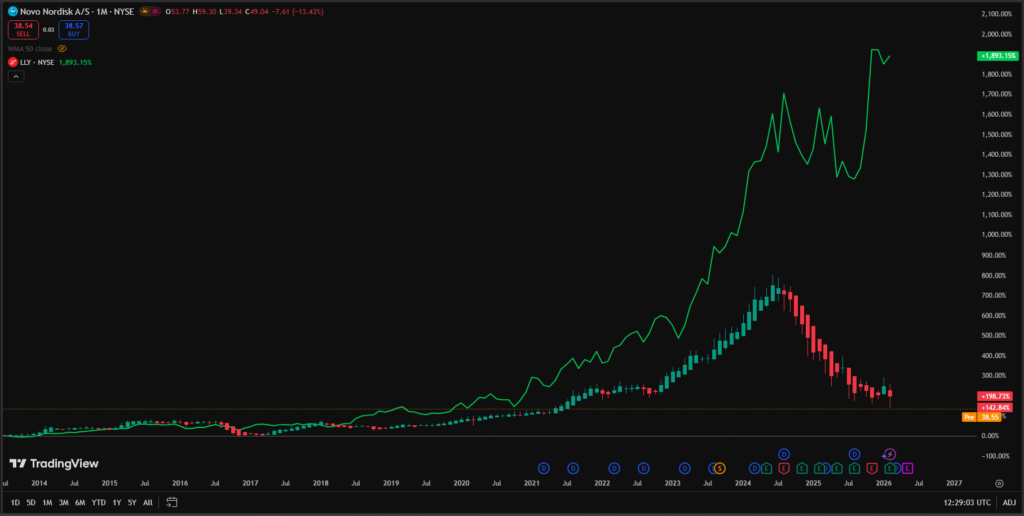

Novo Nordisk (NVO) shares plummeted over 21% in 48 hours following REDEFINE 4 trial data, where CagriSema showed a 23% weight loss compared to Eli Lilly’s Zepbound at 25.5%. Despite the market’s knee-jerk reaction, fundamental analysis reveals a 2026 P/E of 11x, a massive discount compared to Lilly’s 30x. With a robust pipeline including oral Wegovy and the triple agonist UBT251, the long-term investment thesis remains intact.

The trading sessions of yesterday and today in New York and Copenhagen felt like a coordinated capitulation. Watching a titan like Novo Nordisk (NVO) retreat more than 17% in a single day, followed by an additional 4% slide today, is the kind of event that tests any investor’s conviction. However, as a senior analyst and a shareholder who holds NVO in my personal portfolio, I view this noise with the necessary coldness to distinguish volatility from fundamental deterioration. The market is reacting viscerally to a 2.5 percentage point weight-loss delta, ignoring clinical complexity and the financial fortress of a company that still dominates the global obesity duopoly.

In this article, I will dissect the reasons behind this “crash,” analyze the recent strategic defense from CEO Mike Doustdar, compare valuation metrics with its arch-rival Eli Lilly (LLY), and explain why, in my view, we are facing one of the most significant value asymmetries in years. If you want to revisit my previous analysis on this company’s resilience, you can check my last post at Novo Nordisk in Free Fall.

1. The REDEFINE 4 Shock: Did CagriSema Truly Disappoint?

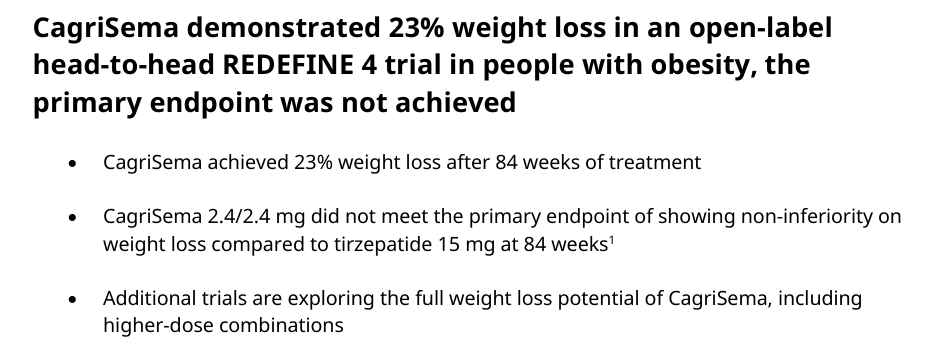

The primary catalyst for the sell-off was the headline results from the Phase 3 REDEFINE 4 trial. CagriSema—a fixed-dose combination of cagrilintide and semaglutide—was widely perceived as Novo Nordisk’s “silver bullet” to reclaim absolute efficacy leadership from Eli Lilly’s Zepbound. The data showed a mean weight loss of 23.0% after 84 weeks, while Lilly’s Tirzepatide (15 mg) achieved 25.5%.

At first glance, the algorithms interpreted this as a clinical defeat. However, it is essential to look at the “fine print” of the report. CEO Mike Doustdar was firm in his defense, calling CagriSema a “fantastic drug” that will boast the strongest weight-loss label at launch, expected early next year.

A critical point that many analysts at firms like Jefferies are overlooking is the open-label design of the study. In an open-label trial, both investigators and participants know which drug is being administered. Historically, this can introduce a psychological bias in favor of the drug that currently holds the “hype” advantage, as Tirzepatide does. Novo’s management suggested that future head-to-head comparisons should be blinded to eliminate this noise. More importantly, the company is already looking toward REDEFINE 11, where higher-dose escalation is expected to push efficacy beyond the 25% threshold by 2027.

2. Doustdar’s Shift and the Oral Wegovy Trump Card

In response to the skepticism regarding CagriSema’s commercial role without clear superiority, Doustdar pivoted the focus toward convenience and portfolio depth. Novo Nordisk is not just an injectables company.

The recent push for the oral version of Wegovy is, in my opinion, the true “game-changer” that the market is ignoring today. With a weight loss efficacy of approximately 17%, there is currently no oral competitor close to this profile. It is the first and best pill in its class. While Eli Lilly focuses on absolute peak potency via injection, Novo is building an access ecosystem: from the oral pill for maintenance to high-potency injectables for initial treatment.

Comparative Data: Obesity Pipeline (2026 Outlook)

| Asset | Company | Mechanism | Efficacy (Weight Loss) | Status |

| CagriSema | Novo Nordisk | GLP-1 + Amylin | 23.0% | Launch 2027 |

| Zepbound | Eli Lilly | GLP-1 + GIP | 25.5% | Marketed |

| Oral Wegovy | Novo Nordisk | GLP-1 | ~17.0% | Submission Phase |

| UBT251 | Novo/TUL | Triple Agonist | 19.7% (24 weeks) | Phase 2 Results |

| Amycretin | Novo Nordisk | Oral GLP-1/Amy | Promising | Early Clinical |

3. The Obesity Market: A Blue Ocean for Two Giants

A common mistake in the current NVO vs. LLY debate is treating the competition as a zero-sum game. The global obesity market is so vast—with estimates pointing to over a billion people living with obesity by 2030—that the question isn’t “who has the best drug,” but rather “who can produce the most.”

Currently, only these two companies possess the fill-finish infrastructure, supply chain scale, and logistics to meet this demand. The 17% drop suggests a mass exodus of patients from Novo Nordisk. On the contrary, waiting lists remain the biggest obstacle to revenue, not marginal efficacy differences. Novo has invested billions into manufacturing expansion, ensuring that regardless of whether CagriSema is 2% “less potent,” it will be the available option for millions.

4. What the Market Forgot: Diabetes and Beyond

While trading algorithms sell NVO based on obesity trial headlines, I am looking at the consolidated balance sheet. Novo Nordisk is the world leader in diabetes care, a segment that generates massive and predictable cash flow.

Furthermore, the SELECT study has already proven that semaglutide reduces the risk of major adverse cardiovascular events (MACE). This shifts the drug from a “lifestyle product” to a medical necessity that public health systems and private insurers (like those in the US) will be forced to cover. This transition from “weight loss” to “cardiometabolic health” is what will guarantee double-digit growth for the next decade, regardless of quarterly volatility.

5. Fundamental Valuation: 2021 Prices with 2026 Earnings

This is the heart of my investment thesis. We are seeing Novo Nordisk trading at price levels we haven’t seen since 2021/2022. Yet, the company today is a much more powerful financial engine than it was five years ago.

- P/E Ratio: Novo Nordisk is trading at a forward P/E of approximately 11x for 2026 estimates.

- Eli Lilly Comparison: Its main rival, Eli Lilly, trades at a P/E of 30x.

This discrepancy is irrational. Historically, Novo Nordisk has not grown significantly slower than Lilly, and there is no clinical or operational evidence justifying that Lilly should trade at nearly triple the earnings multiple. If we were to value Novo Nordisk at a multiple equal to Lilly’s, the stock price would be around $105 per share. Even with moderate growth expectations, NVO is in “deep value” territory.

6. Technical Analysis and Portfolio Management

Technically, the drop was violent, breaking key psychological support levels. However, we are reaching selling exhaustion zones. The Relative Strength Index (RSI) is in deep oversold territory. Historically, whenever the divergence between NVO and LLY has reached these extremes, a mean reversion has occurred.

I will continue to hold Novo Nordisk in my portfolio. I am not selling; I am monitoring the technical indicators—specifically the RSI and the approach to long-term moving averages—to add to my position. Fundamentals eventually crush sentiment in the long run, and Novo’s fundamentals have never been this cheap.

Frequently Asked Questions (FAQ)

Did CagriSema fail its primary objectives?

Not entirely. While it did not achieve statistical superiority over Tirzepatide in REDEFINE 4, it reached a 23% weight loss, making it one of the most potent drugs globally. The “failure” was strictly relative to inflated market expectations.

Why did Novo Nordisk drop so much despite positive results (23% weight loss)?

The drop is due to the loss of the “efficacy leadership narrative.” Investors fear Eli Lilly will capture the high-performance segment, ignoring that the market is large enough for both and that Novo dominates other segments like oral treatments.

What is NVO’s fair value compared to Eli Lilly?

If Novo Nordisk were valued at the same 30x P/E multiple as Eli Lilly, the fair price per share would be approximately $105, representing massive upside potential from its current 2026 valuation levels.

Conclusion: Panic is the best friend of the value investor. The 20%+ drop in Novo Nordisk is an overreaction to clinical minutiae in a drug-starved market. With a 2026 P/E of 11x, a pipeline that includes oral Wegovy and new triple agonists like UBT251 (which showed 19.7% loss in just 24 weeks), my conviction is unchanged. NVO is a financial fortress on sale. I am waiting for the technical stabilization signal to “back up the truck.”

Disclaimer: This article reflects my personal opinion and investment positions. It does not constitute personalized financial advice. Stock market investments involve risk of loss. Always consult official reports from authorities like the SEC or the ECB.

Related posts:

Is Novo Nordisk (NVO) Still a Buy in 2026? My Deep Dive into the Giant Curing Obesity

Is Novo Nordisk (NVO) Still a Buy in 2026? My Deep Dive into the Giant Curing Obesity

The Civil War at the Federal Reserve: Is Jerome Powell’s Resistance the Last Stand for Economic Stability?

The Civil War at the Federal Reserve: Is Jerome Powell’s Resistance the Last Stand for Economic Stability?

Trade War 2.0 Greenland: How to Shield Your Portfolio Against New NATO Tariffs and Arctic Volatility

Trade War 2.0 Greenland: How to Shield Your Portfolio Against New NATO Tariffs and Arctic Volatility

2026 AI IPOs: The Triumph of FOMO or the Next Dot-Com Burst?

2026 AI IPOs: The Triumph of FOMO or the Next Dot-Com Burst?