In 2025, Netflix earnings solidified its dominance with revenue of $45.2 billion (+16% YoY) and an operating margin of 29.5%. With 325 million subscribers, the focus shifts to 2026, projecting revenue up to $51.7 billion and the strategic integration of Warner Bros. Discovery through an “all-cash” transaction. Despite robust growth, a P/E ratio of 26x and a 30% retreat from all-time highs suggest rigorous investor selectivity.

In the volatile world of financial markets, few names evoke as much debate over value and growth as the Los Gatos giant. Today, I am taking a close look at Netflix earnings recent Q4 2025 , a period I consider to be a true watershed moment for the company’s investment thesis heading into 2026. Analyzing the 2025 annual report and future guidance, I see a company that has not only survived the “streaming wars” but is actively attempting to rewrite the rules of the game through massive acquisitions and new business verticals. However, as a senior analyst, I cannot ignore the elephant in the room: the stock has already pulled back more than 30% from its record highs, where it boasted a P/E (Price-to-Earnings) ratio that I would consider prohibitive for any rational investor. Even with the recent 5% slide in after-hours trading following this announcement, the ticker is currently trading at 26 times this year’s expected earnings—a multiple that, in my personal opinion, remains extremely demanding and leaves little room for operational error.

1. The 2025 Financial Radiography: Revenue and Margins on the Rise

Dissecting the numbers presented at the close of 2025, it is impossible not to be impressed by the operational execution of the management team led by Ted Sarandos and Greg Peters. The company delivered a total revenue of $45.2 billion, representing 16% year-over-year growth (or 17% on a constant-currency basis). What stands out most to me, however, is the margin expansion. Netflix closed the year with an operating margin of 29.5%, a jump of 3 percentage points compared to 2024.

This increase in profitability is no accident. I see a clear paradigm shift here: Netflix has transitioned from being a “cash-burning machine” to a formidable cash generator. Free Cash Flow (FCF) reached $9.5 billion in 2025, exceeding initial forecasts of $9 billion. For 2026, management has already signaled an even more ambitious goal of $11 billion in FCF. This financial robustness is what allows the company to pursue large-scale M&A (Mergers and Acquisitions) without compromising its long-term solvency.

| Financial Metric | 2024 (Actual) | 2025 (Actual) | 2026 (Projected) |

| Total Revenue | ~$39B | $45.2B | $50.7B – $51.7B |

| YoY Growth | – | 16% | 12% – 14% |

| Operating Margin | 26.7% | 29.5% | 31.5% |

| Paid Subscribers | ~282M | 325M | – |

| Free Cash Flow | $6.9B | $9.5B | ~$11B |

2. The Advertising Engine and the 325 Million Member Milestone

One of the pillars sustaining growth in 2025 was undoubtedly the advertising segment. In its third year of operation, ad revenue skyrocketed more than 2.5x, surpassing $1.5 billion. For 2026, the company expects this figure to roughly double again. I view this strategy as fundamental to maintaining subscriber base growth. By crossing the historic milestone of 325 million paid memberships in Q4 2025, Netflix proved there is still room for expansion, even in saturated markets.

My analysis suggests that advertising acts as a retention net. By offering more affordable plans supported by ads, the company reduces churn and attracts a demographic that was previously financially out of reach. Furthermore, the integration of AI tools to help advertisers create personalized ads based on Netflix IP, initiated in 2025, promises to increase the value of ad inventory in 2026. However, the market seems to have already priced in much of this optimism, which explains the lukewarm—and even negative—reaction of the stock following these robust data points.

3. The Big Bet: The Warner Bros. Acquisition and the All-Cash Future

Perhaps the most impactful news for the long-term investor is the progress on the Warner Bros. (WBD) acquisition. In January 2026, Netflix announced a structural change to the deal: the transaction will now be entirely all-cash, valued at $27.75 per WBD share. This is a bold move that signals tremendous confidence in its balance sheet. To fund this operation, Netflix secured commitments for a bridge loan facility that reached $59 billion, later adjusted to $42.2 billion as they utilize their own cash reserves.

From my technical perspective, the purchase of Warner Bros. isn’t just about scale; it’s about content and IP. Adding the WB library, film and TV studios, and especially HBO Max, will allow Netflix to offer unprecedented variety and quality. However, this move forces the suspension of the share buyback program to accumulate capital, which removes a key technical support for the stock price in the short term. Integration risk is real, and the market is watching closely to see if Netflix can maintain its projected 31.5% margins for 2026 while absorbing the operational costs of a legacy giant like Warner Bros.

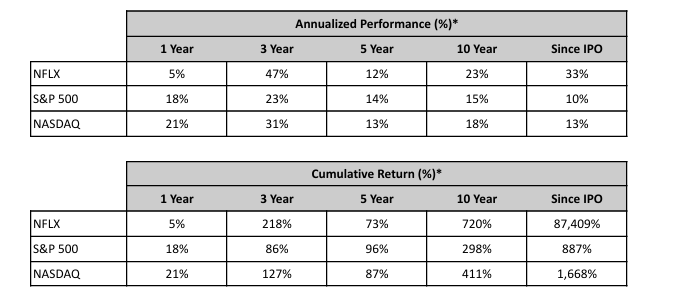

4. Valuation Analysis: The 26x P/E and the Margin of Safety

Now, we get to the heart of my concern as an analyst: market valuation. It is a fact that Netflix stock has retreated significantly from its peaks of euphoria. Seeing the ticker drop 30% from its highs is a clear sign that the market is re-evaluating growth multiples in the tech sector. When the stock was at the top, the P/E was, frankly, absurd—a reflection of the extreme euphoria in market sentiment that rarely ends well for the retail investor.

Currently, with the Netflix results in hand and 2026 projections, we are working with a forward P/E of 26x. While it seems more reasonable than in the past, it remains a “luxury” multiple. In an environment where interest rates may not fall as fast as expected and with gross debt at $14.5 billion (prior to consolidating the WBD acquisition), the demand for execution is total. Any miss in subscriber growth or a failure to double ad revenue could lead to further multiple contraction. I am positioned with cautious optimism; Netflix is an extraordinary company, but the current price still demands that everything goes perfectly.

5. The Future Beyond Streaming: Live, Gaming, and Podcasting

To justify its 26x multiple, Netflix is expanding beyond traditional film and series streaming. The report points to massive investment in:

- Live Programming: The success of events like the Anthony Joshua fight and the NFL Christmas games in 2025 paved the way for the World Baseball Classic (WBC) in Japan in 2026, where Netflix will stream all 47 games.

- Gaming: The launch of cloud-first games for TV, such as the newly announced FIFA soccer simulator, aims to increase retention and the value of watch time.

- Video Podcasts: In partnership with Spotify and Barstool Sports, the company is aggressively entering the video podcast format, seeking to capture user attention at different points throughout the day.

These initiatives are crucial because they attack leisure time on multiple fronts. However, they also put Netflix on a direct collision course with giants like YouTube (Google) and Amazon, which already have very mature sports and video ecosystems.

FAQ: Frequently Asked Questions on Netflix Earnings

What was Netflix’s revenue growth in 2025?

Netflix reported revenue of $45.2 billion in 2025, a 16% year-over-year increase, driven by growth in memberships and advertising.

What is the status of Netflix’s acquisition of Warner Bros?

The acquisition is underway and was recently amended to a 100% all-cash transaction at $27.75 per WBD share, aiming to accelerate the company’s content strategy.

Will Netflix continue to buy back shares in 2026?

No. The company announced a temporary suspension of share buybacks to preserve cash and finance the acquisition of Warner Bros. Discovery.

What is the projected operating margin for 2026?

Netflix expects to reach an operating margin of 31.5% in 2026, up from the 29.5% recorded in 2025, despite the acquisition costs.

Conclusion: A Fortress in the Making, But at a Premium Price

In summary, Netflix’s results at the end of 2025 show a company in full command of its operational faculties. The transition to a hybrid model of subscription and advertising is bearing fruit, and the audacity of acquiring Warner Bros. could solidify its place as the “public utility” of global entertainment. However, as a financial writer, it is my duty to warn about valuation risk. The 5% drop in after-hours and the 30% retreat from highs are signals that the market is no longer willing to pay any price for growth. A 26x P/E for 2026 is demanding, especially considering that revenue growth is expected to slow slightly to the 12-14% range. My personal view is one of guarded optimism: Netflix is the undisputed leader, but the savvy investor should wait for entry points that offer a real margin of safety—something that, even after the recent dips, still seems scarce at this price level.

Related posts:

The Civil War at the Federal Reserve: Is Jerome Powell’s Resistance the Last Stand for Economic Stability?

The Civil War at the Federal Reserve: Is Jerome Powell’s Resistance the Last Stand for Economic Stability?

Trade War 2.0 Greenland: How to Shield Your Portfolio Against New NATO Tariffs and Arctic Volatility

Trade War 2.0 Greenland: How to Shield Your Portfolio Against New NATO Tariffs and Arctic Volatility

The Greenland Crisis: How Trump’s New Tariffs Could Wreck Your Tech Portfolio Today

The Greenland Crisis: How Trump’s New Tariffs Could Wreck Your Tech Portfolio Today

The End of the Dovish Illusion: Why the January 2026 FOMC Meeting Left Markets in Limbo

The End of the Dovish Illusion: Why the January 2026 FOMC Meeting Left Markets in Limbo