On February 17, 2026, General Mills (GIS) stock dropped over 6% following a downward revision of its fiscal 2026 guidance at the CAGNY Conference. The company now forecasts organic net sales between -1% and 0% and a decline in adjusted EPS of 2% to 1%. Despite the volume pressure and consumer fatigue, the 5.44% dividend yield and leadership in the pet and snack categories maintain a strong long-term bull case for defensive investors.

The stock market is a stern teacher, and today, it delivered a harsh lesson to those who underestimated the current fragility of the consumer staples sector. As a senior market analyst and investor who has navigated several cycles of volatility, I watched General Mills (GIS) stock experience a significant correction of over 6% during early trading. This move was a visceral reaction to the company’s decision to slash its fiscal 2026 outlook. The question keeping investors awake today is whether this dip is a structural red flag or a temporary hurdle for a centenary giant. My stance remains unwavering: I am holding my position. Much like my recent decision to double down on S&P Global during its 10% dip, I view this GIS correction as a valuation adjustment in a transition year, rather than a collapse of the underlying business model.

1. A Century of Resilience: Understanding the General Mills Moat

To analyze the current situation of General Mills (GIS) stock, one must first appreciate the architectural strength of its business. This is not just a food company; it is an institution of American capitalism. Founded as the Washburn-Crosby Company in the 19th century, General Mills evolved from a simple flour miller in Minneapolis into a global powerhouse of branded consumer goods. Its history is a masterclass in adaptation.

I have always been fascinated by how the company manages its vast portfolio. We are talking about brands that have become synonymous with their categories. Cheerios isn’t just a cereal; it’s a global breakfast standard. Nature Valley created the granola bar category as we know it. From the iconic Pillsbury Doughboy to the premium indulgence of Häagen-Dazs, the company has successfully captured “share of stomach” across various demographics and price points. This dominance provides a competitive moat that is incredibly difficult to breach. Even in a 2026 landscape where private labels are gaining ground, the brand equity of GIS remains a formidable barrier to entry.

The Strategic Pivot: The Blue Buffalo Era

Perhaps the most significant move in the company’s recent history was the 2018 acquisition of Blue Buffalo. By entering the high-growth “pet humanization” market, General Mills fundamentally changed its growth profile. In my technical view, the Pet segment has become the company’s “growth engine,” often offsetting the slower growth seen in traditional North American Retail (NAR). Despite the temporary volume headwinds mentioned today, the long-term trend of pet owners prioritizing premium nutrition remains a secular tailwind that I believe the market is currently discounting too heavily.

2. The February 2026 Catalyst: Decoding the Outlook Cut

The volatility we witnessed today stems directly from the CAGNY (Consumer Analyst Group of New York) conference. The management team, led by CEO Jeff Harmening and CFO Kofi Bruce, provided an update that sent algorithmic traders into a selling frenzy. They admitted that the “consumer environment remains challenging,” a phrase that has become a euphemism for price-weary shoppers switching to cheaper alternatives.

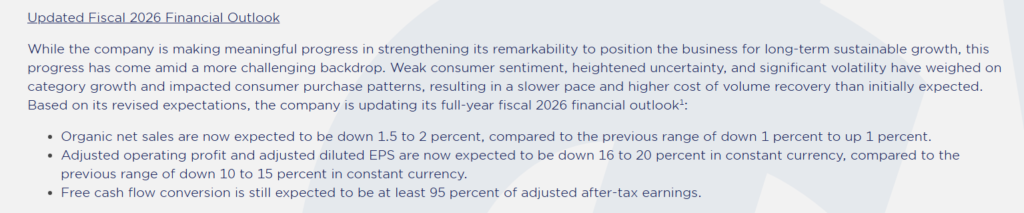

The Revised Numbers for Fiscal 2026

Let’s look at the cold, hard data. The company had to walk back its previous optimism, providing the following revised guidance:

- Organic Net Sales: Previously expected at 0% to +1%, now revised to -2% to -1.5%.

- Adjusted Diluted EPS: Now forecasted to decline between 20% and 16%, a sharp contrast to previous hopes of modest growth.

In my professional opinion, this cut is a classic “kitchen-sink” move. Management is lowering the bar now to ensure they can beat it later in the year. The market’s 6% reaction reflects the disappointment of growth-oriented funds, but for a value investor, these moments often represent the “maximum point of pessimism” where the best entries are found. The pressure on volumes is real, but it is a sector-wide phenomenon, not a GIS-specific failure.

3. Fundamental Analysis: ROIC, Margins, and the 10-K Insights

When a stock like General Mills (GIS) drops, I dive straight into the 10-K filings and the Return on Invested Capital (ROIC). The 2025 annual report showed a company that, while facing headwinds, remains a lean machine.

ROIC and Capital Allocation

One of the metrics I hold most dear is the ROIC. General Mills has historically maintained a double-digit ROIC, which is a testament to its efficient use of capital. Even with the forecasted earnings dip in 2026, the company’s Holistic Margin Management (HMM) program is expected to deliver significant productivity savings. These savings are the “fuel” that allows GIS to reinvest in marketing and innovation without destroying its bottom line.

I see a company that is not simply standing still. It is divesting non-essential assets (such as the recent sale of the yogurt business in North America) and focusing on high-margin areas. This ‘portfolio restructuring,’ as Harmening calls it, is essential to maintain a ROIC around 10%, which is high for this type of company. If they manage to successfully navigate the current drop in volumes, the leaner portfolio will be much more profitable when consumers eventually return to brand loyalty.

4. The Dividend Fortress: Why Income Investors Should Take Notice

If there is one reason to keep General Mills (GIS) stock in a core portfolio, it is the dividend. We are talking about one of the most reliable dividend payers in the history of the New York Stock Exchange.

A 127-Year Legacy

General Mills and its predecessor have paid dividends without interruption for 127 years. Let that sink in. This company has paid through the Great Depression, two World Wars, the 2008 financial crisis, and the 2020 pandemic.

With today’s drop in the stock price to the $45 range, the Dividend Yield has risen to approximately 5.44%. In a world where the Fed is still dealing with interest rate volatility, a 5.44% yield from a company of this kind of prestige is incredibly attractive. The Dividend Payout Ratio remains healthy, usually around 50-60%, which means that even with a 20% drop in earnings per share, the dividend can still be maintained. For my personal strategy, I see these dividends as a ‘reinvestment engine’ that allows me to buy more shares while the price is depressed.

5. Technical Valuation: P/E Ratios and Entry Points

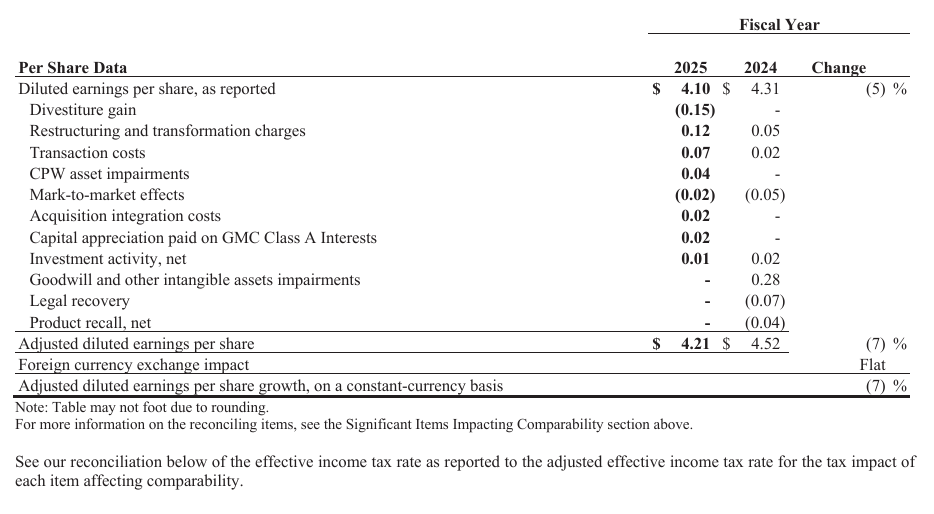

Now, calculating a 20% drop in EPS on the 2025 results ($4.21), we get an EPS for 2026 of around $3.37. Thus, the stock is trading at a forward P/E for 2026 of approximately 13x.

Comparing this with its five-year average P/E of about 17x, it is clear that the market has already priced in a significant amount of negative news. Is the stock cheap? Yes. Could it go lower? Possibly. Support levels seem to be forming around $40-37. If it reaches that range, the yield will reach 6.5%, which is historically very high for this type of stock.

6. Personal Conviction: Why I am Holding and Refortifying

I currently hold General Mills in my portfolio, and today’s news does not change my long-term thesis. In fact, it reinforces the need for “boring” defensive stocks. I believe it is essential to have a percentage of the portfolio in consumer essentials. When tech gets frothy or the economy stutters, people still need to feed their families and their pets.

I am keeping my GIS shares because:

- Brand Power: The current consumer pivot to private labels is cyclical, not structural. Once inflation stays settled, brand loyalty usually recovers.

- Pet Segment Potential: Blue Buffalo is still the best-in-class brand in a high-margin sector.

- Capital Returns: Between dividends and share buybacks, GIS remains committed to returning value to me, the shareholder.

For those looking to verify the official data, I highly recommend reviewing the latest General Mills Investor Relations press releases.

Frequently Asked Questions (FAQ)

1. Why did General Mills (GIS) stock drop 6% today?

The drop was caused by a downward revision of the fiscal 2026 outlook. The company now expects lower sales and profits than previously forecasted due to a “challenging consumer environment.”

2. Is the General Mills dividend safe after the profit warning?

Yes. General Mills has an uninterrupted 127-year dividend history. Its payout ratio remains sustainable, and the company generates strong free cash flow even during periods of earnings pressure.

3. What is the current P/E ratio for GIS?

Following the price drop on Feb 17, 2026, the stock trades at a forward P/E of approximately 14.5x to 15x, which is below its historical average.

4. What is the revised guidance for organic sales?

The company now expects organic net sales to range from -1% to 0% for the full fiscal year 2026.

Conclusion: The Long Game in Consumer Staples

In conclusion, the 6% drop in General Mills (GIS) shares today is a classic example of the market overreacting to short-term guidance adjustments. While the EPS outlook of up to -20% is not something to celebrate, it is certainly not a reason for a panic sell either. The company’s enormous competitive advantage, its ‘dividend fortress’ status, and its strategic focus on high-margin categories such as Pet Products and Snacks provide a safety net that few other companies can match.

As an investor, I embrace these moments of volatility. They are the times when “weak hands” fold and disciplined investors build their wealth. I will continue to hold my GIS position, collect my 5.44% yield, and wait for the “Accelerate” strategy to bear fruit as the consumer cycle turns. Patience in the market is often just another word for profit.

Disclaimer: This article represents my personal opinion and analysis. It does not constitute financial advice. Investing in the stock market involves risk, and you should perform your own due diligence or consult with a certified financial advisor before making any investment decisions.

Related posts:

The Civil War at the Federal Reserve: Is Jerome Powell’s Resistance the Last Stand for Economic Stability?

The Civil War at the Federal Reserve: Is Jerome Powell’s Resistance the Last Stand for Economic Stability?

Trade War 2.0 Greenland: How to Shield Your Portfolio Against New NATO Tariffs and Arctic Volatility

Trade War 2.0 Greenland: How to Shield Your Portfolio Against New NATO Tariffs and Arctic Volatility

The Greenland Crisis: How Trump’s New Tariffs Could Wreck Your Tech Portfolio Today

The Greenland Crisis: How Trump’s New Tariffs Could Wreck Your Tech Portfolio Today

2026 AI IPOs: The Triumph of FOMO or the Next Dot-Com Burst?

2026 AI IPOs: The Triumph of FOMO or the Next Dot-Com Burst?