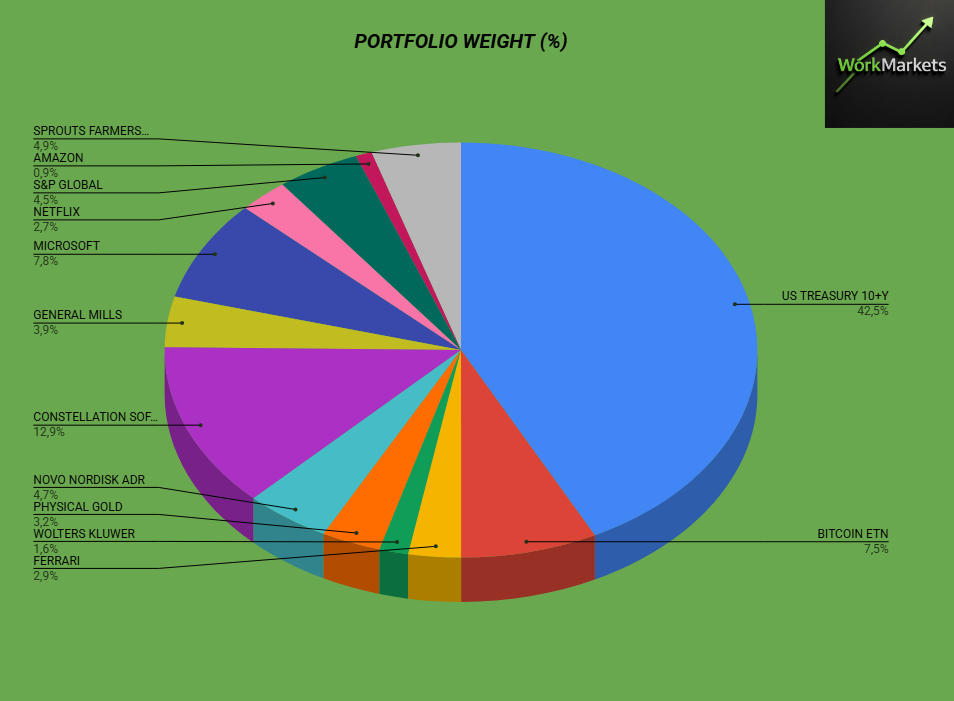

In April 2026, my portfolio strategy prioritizes capital preservation and fixed-income yields, allocating 42.6% to US Treasuries 10+Y. A strategic entry into Physical Gold at $4,400/oz serves as a core inflationary hedge. Despite volatility in Bitcoin ETN (-20% net profitability) and Novo Nordisk (-23%), I am maintaining high-conviction positions in Microsoft (7.8%) and Constellation Software (12.9%), while scouting Meta, Mercado Libre, and Tesla for potential entries during deeper market corrections.

Managing an investment portfolio in 2026 requires more than just guts; it demands a surgical reading of the macroeconomic landscape and an iron discipline to ignore the daily noise of the 24-hour news cycle. Following my February 2026 portfolio close, where I began anticipating a defensive rotation, I decided to act with total conviction. My current portfolio strategy reflects a posture of cautious optimism, where preserving purchasing power has become the central pillar of my wealth management. In this article, I will dissect the reasons why I have drastically increased my exposure to long-duration US sovereign debt, the logic behind my gold entry, and how I plan to use my proprietary stock-picking methodology to capitalize on opportunities brewing in names like Meta or Tesla.

1. The Supremacy of Fixed Income: The 42.6% Giant in US Treasuries

Looking at my Portfolio Weight chart, it is impossible to ignore the massive 42.6% allocation to US Treasury 10+Y. Many retail analysts might question why a growth-oriented investor would keep nearly half of their capital in American sovereign debt. The answer is straightforward: the risk-reward profile in 2026 has fundamentally shifted. With Federal Reserve (Fed) rates stabilizing at a higher plateau to combat persistent inflation, long-duration Treasuries now offer not just a safe haven, but a real yield that we haven’t seen in decades.

I firmly believe we are at an inflection point where principal protection is just as vital as the pursuit of alpha. This massive bond position acts as the ballast of my ship. While the equity market exhibits erratic volatility, my Treasuries ensure predictable cash flow and significant capital appreciation potential should macroeconomic data signal a deeper recession—which would force the Fed into aggressive rate cuts. It is a bet on convexity: if rates fall, the face value of these bonds will skyrocket. If rates stay flat, the coupon remains my safe harbor.

2. Gold at $4,400: Why I Entered Now

Another significant shift from my February portfolio is the inclusion of Physical Gold (3.2%). As I detailed in my report on strategically entering gold at $4,400, my thesis is rooted in fiat debasement and the geopolitical tensions that continue to plague global supply chains in 2026.

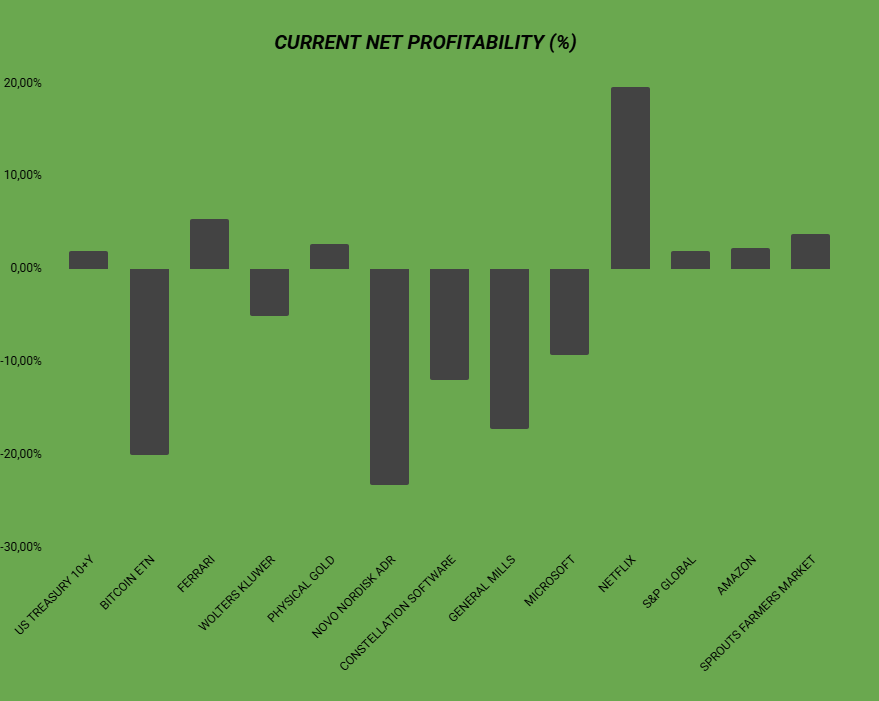

Entering gold at this price level might seem like “buying the top” to the uninitiated, but I view it as a hedge against central bank error. Historically, gold is the only asset without counterparty risk. In my net profitability chart, gold is already showing a slight positive trend, validating the timing of the entry. I don’t look to gold to get rich; I look to it to ensure that if the traditional financial system faces a liquidity squeeze or a crisis of confidence in the dollar, my net worth has a tangible, time-tested reserve of value.

Allocation Comparison: February vs. April 2026

To help you visualize the scale of these adjustments, I’ve prepared the table below comparing the relative weights of my primary asset classes:

| Asset / Class | Feb 2026 Weight (%) | Apr 2026 Weight (%) | Variance (%) | Strategic Note |

| US Treasuries 10+Y | 35.0% | 42.6% | +7.6% | Increased defensive yield. |

| Constellation Software | 14.2% | 12.9% | -1.3% | Passive reduction via relative valuation. |

| Bitcoin ETN | 8.5% | 7.4% | -1.1% | Price drop (Short-term bearish). |

| Physical Gold | 0.0% | 3.2% | +3.2% | New strategic entry. |

| Microsoft | 8.0% | 7.8% | -0.2% | Core technology holding. |

| Novo Nordisk | 5.5% | 4.7% | -0.8% | Suffering from sector-wide correction. |

3. Bitcoin and Big Tech: Growth Pains and Staying the Course

Observing the Current Net Profitability (%) chart, it’s clear that not everything is coming up roses. My Bitcoin ETN shows a negative return of approximately 20%. Similarly, Novo Nordisk ADR is currently my largest performance detractor, with a drop exceeding 23%. However, this is where investor psychology separates the pros from the amateurs.

I do not sell high-quality assets simply because the price dropped. On the contrary, I have slightly increased my position in Bitcoin ETFs during recent dips. The thesis of Bitcoin as “digital gold” remains intact. In 2026, with the definitive institutionalization of the asset by the likes of BlackRock and Fidelity, these corrections are, in my view, generational accumulation opportunities.

Regarding Novo Nordisk, the correction reflects a reset of expectations after the massive hype of previous years. However, the company’s fundamentals and its dominance in the metabolic treatment market remain unshakable. I am holding the position (4.7% of the portfolio) with patience, waiting for the market to refocus on free cash flow generation rather than mere momentum.

4. Case Study: Constellation Software and Microsoft

Constellation Software (CSU) continues to be the “crown jewel” of my equity portfolio, representing 12.9% of my holdings. The reason is simple: their business model of acquiring niche Vertical Market Software (VMS) companies is a near-perfect capital compounding machine. Even in a high-interest-rate environment, CSU manages to acquire companies at attractive multiples using its own operating cash flow. It is the epitome of what I look for in my stock-picking strategy.

Microsoft (7.8%), meanwhile, is my bet on Artificial Intelligence infrastructure. Although current net profitability is slightly negative (-9%), the integration of Copilot and Azure’s dominance in the cloud market make MSFT an indispensable asset. By 2026, AI has transitioned from a promise to a critical component of global GDP, and Microsoft holds the keys to that kingdom.

5. My Watchlist for the Next Correction: Meta, MELI, and Tesla

Many ask me: “With 42% in Treasuries, what are you going to do with the cash?” The answer is: wait for the right pitch. I am closely monitoring three specific companies for capital allocation if we see a more pronounced “sell-off”:

- Meta (Facebook/Instagram/Reality Labs): Their ability to generate massive cash flows and their leadership in spatial computing hardware make them extremely attractive if their earnings multiple drops to historically low levels.

- Mercado Libre (MELI): The Latin American giant continues to grow at impressive rates. If there is a flight from emerging markets that unfairly penalizes the stock price, I will be there to buy.

- Tesla: Elon Musk’s company remains the barometer for tech risk sentiment. If the correction deepens and Tesla hits key technical support levels, I intend to initiate a tactical position focused on its competitive advantage in FSD (Full Self-Driving) and energy storage.

As I mentioned in previous reports and following data from the CME FedWatch Tool, the probability of rates staying “higher for longer” through the end of 2026 remains high. This means liquidity will be scarce, and those who have “dry powder” (as I do through Treasuries and Cash) will be king when it comes time to buy luxury assets at fire-sale prices.

Frequently Asked Questions (FAQ)

Why do you have nearly half your portfolio in US Treasuries?

In 2026, Treasuries offer an attractive real yield and protection against extreme stock market volatility. They serve as my primary defensive hedge.

Isn’t buying Gold at $4,400 risky?

Gold is wealth insurance. At $4,400, the price reflects accumulated inflation and global instability. The goal is not a quick flip, but the preservation of purchasing power.

What should I do about the 20% drop in Bitcoin?

I am sticking to my long-term thesis. According to my trading strategy, pullbacks in fundamentally high-quality assets are buying opportunities, not reasons to panic.

Which stocks do you plan to buy next?

I am focused on Meta, Mercado Libre (MELI), and Tesla, but only if the market offers a price correction that justifies the necessary margin of safety.

Conclusion: Discipline Over Emotion

My April 2026 portfolio is a direct reflection of my evolution as an investor. I have shifted from an aggressive stance in 2024/2025 to a robust and diversified strategy that prioritizes resilience. The 20% return on Netflix and gains in Ferrari (2.9% weight) show that there is still room for selective growth, but the 42.6% in Treasuries is what allows me to sleep soundly at night.

Investing isn’t about being right all the time; it’s about surviving to invest another day. By balancing the cutting-edge technology of Microsoft and Constellation with the millennial security of gold and the solidity of US bonds, I am prepared for whatever scenario the rest of 2026 throws our way. If the market crashes, I have the liquidity and defensive assets to swap for cheap stocks. If the market rallies, my equity positions ensure I won’t be left behind.

To track the real-time evolution of the yields that anchor the majority of my portfolio, I recommend consulting the official data directly from the source:

External Link: Daily Treasury Par Yield Curve Rates – U.S. Department of the Treasury

Disclaimer: This article reflects only my personal opinion and my individual investment strategy as of April 2026. Nothing written here constitutes a recommendation to buy or sell financial assets. Stock market investments involve risks of capital loss. Always consult a certified financial advisor before making investment decisions.