General Mills (GIS) reported its fiscal 2026 third-quarter results today, March 18, 2026, showing net sales of $4.4 billion (an 8% decline) and an adjusted EPS of $0.64 (a 37% drop). Despite severe margin contraction driven by “remarkability” investments and strategic divestitures (Yogurt and Brazil), the company reaffirmed its full-year guidance. With the stock sliding 3% today and nearly 60% from its all-time highs, the market remains skeptical of the portfolio’s restructuring efficacy.

1. The General Mills Earnings Earthquake: A Cold-Blooded Analysis

I woke up today to my Bloomberg terminal flashing in aggressive shades of red. The fiscal third-quarter results for 2026 from General Mills have just been released, and for those of us who are shareholders, the initial reading is, at the very least, challenging. In the opening of this analysis, I want to be blunt: General Mills is navigating one of the most critical phases in its century-long history, attempting to balance an aggressive portfolio restructuring with inflationary pressures that refuse to grant the consumer any relief.

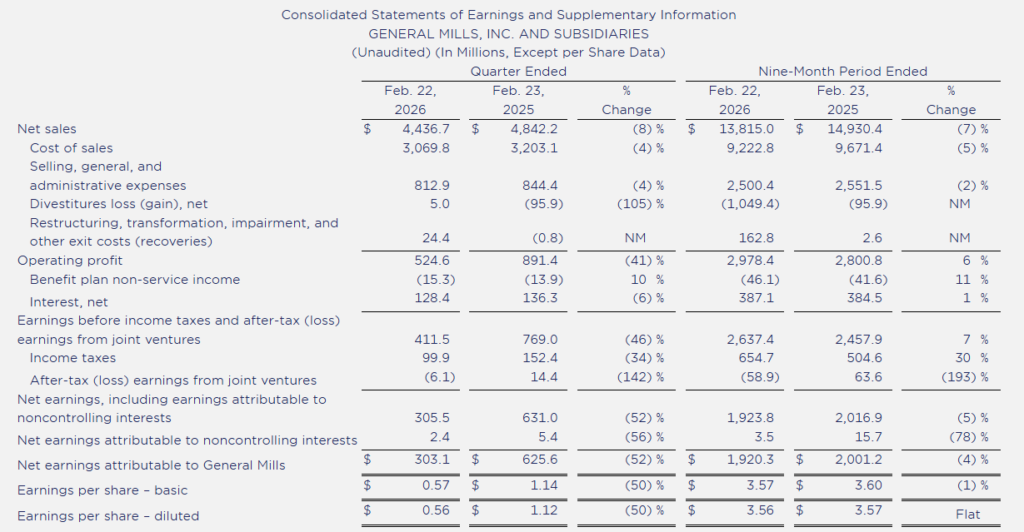

Net sales settled at $4.4 billion, representing an 8% drop on a reported basis. If we look at organic sales, the decline was 3%. What this tells me, as both an analyst and an investor, is that the company isn’t just suffering from the sale of assets—such as the North American yogurt operations—but also from a genuine struggle to maintain volume across its core brands. The market reacted with an immediate slide of nearly 3% in the early hours of trading, deepening a cycle of pain that has already dragged the ticker down nearly 60% from its historical highs.

I hold GIS in my personal portfolio, as you can see in my February 2026 portfolio close, and I won’t hide that this level of depreciation tests any fundamentalist investor’s conviction. However, in finance, price is what you pay; value is what you get. Are we facing a “value trap” or a generational buying opportunity? Let’s dissect the numbers to find the answer.

2. Revenue, EPS, and Crushed Margins: Where is the Floor?

A detailed look at the official earnings report reveals severe profitability erosion. Diluted Earnings Per Share (EPS) stood at $0.56, a brutal 50% collapse compared to the same period last year. Even adjusting for non-recurring items, the adjusted EPS of $0.64 represents a 37% decline in constant currency.

Why did profitability take such a hit? The answer lies in what CEO Jeff Harmening calls the “Remarkability Playbook.” The company is investing heavily in marketing and innovation to make its brands “notable” again in a saturated market. In the short term, this means SG&A (Selling, General, and Administrative) expenses spiked while revenues were falling. As an investor, I have to ask: Will this investment generate the expected return, or are we simply burning cash to defend market share?

Comparative Table: Q3 2026 vs. Q3 2025 Performance

| Financial Metric | Q3 2026 (Current) | Q3 2025 (Previous) | Variation (%) |

| Net Sales | $4.4 Billion | $4.8 Billion | -8% |

| Organic Sales | -3% | +1% | -400 bps |

| Adj. Operating Profit | $547 Million | $804 Million | -32% |

| Adjusted EPS | $0.64 | $1.01 | -37% |

| Net Debt/EBITDA | 3.1x | 2.8x | +10.7% |

This table illustrates the magnitude of the challenge. The 32% contraction in adjusted operating profit is the data point scaring trading algorithms the most. When operating profitability falls faster than revenue, we are looking at negative operating leverage—something the market punishes severely, which is exactly why we see the stock melting down consistently.

3. Selling the Brazil Business: Strategic Pivot or Desperation?

Yesterday, March 17, the company surprised the market by announcing the sale of its Brazilian operations to 3corações. This move includes iconic brands such as Yoki and Kitano. Analyzing the official divestiture slides, it’s clear that General Mills is determined to pivot toward higher-margin categories like super-premium ice cream (Häagen-Dazs), Mexican food (Old El Paso), and pet food (Blue Buffalo).

The Brazil business contributed approximately $350 million to fiscal 2025 net sales. By divesting these operations, the company implicitly admits it failed to achieve sufficient scale or profitability in the South American market. From my perspective, this “portfolio cleaning” is necessary. General Mills had become a conglomerate that was too heavy and inefficient. Selling lower-margin assets to reduce debt and focus on high-yield segments is the right path, albeit a painful one in the near term.

4. Dividends and Share Buybacks: The Investors’ Safe Haven

Despite the turbulent macro environment, General Mills remains a cash-flow machine. Management reaffirmed its commitment to shareholders. Over the first nine months of fiscal 2026, the company has already returned significant capital:

- Dividends: The current dividend yield, given the stock price collapse, is reaching historically high levels, nearing 5%. For an income investor, this is a level that is becoming impossible to ignore.

- Share Buybacks: The company continues to repurchase shares, which helps support long-term EPS by reducing the float. However, I question whether, with debt levels ticking up slightly, it wouldn’t be more prudent to focus on balance sheet deleveraging in this persistent high-interest-rate environment.

Many Wall Street analysts are arguing that the dividend is at risk. I disagree. Free Cash Flow generation is still robust enough to cover payments, but the margin of safety is undeniably thinner than it was a year ago.

5. 2026 Guidance: A Vote of Confidence in “Remarkability”

Surprisingly, Jeff Harmening and his team reaffirmed the full-year fiscal 2026 guidance. They expect the fourth quarter to offset some of the current losses, benefiting from an easier year-over-year comparison and the first fruits of their brand investments.

The company’s vision for the future rests on the “Accelerate” strategy. They believe that by removing “dead weight” (the Yogurt business and Brazil), the company will emerge as a leaner organization with higher pure margins. However, the market is an anticipation mechanism, and right now, it simply doesn’t buy that narrative. The 60% drop from the highs reflects total pessimism regarding organic growth capacity in consumer staple categories, where private labels are aggressively stealing market share.

6. Why has the Stock Dropped 60%, and What Does Technical Analysis Say?

A 60% decline doesn’t happen by accident. It is the sum of several factors:

- Shifting Habits: Consumers are fleeing ultra-processed foods.

- Competition: Private labels from retailers like Walmart and Costco are crushing brand loyalty.

- Debt Burden: Past acquisitions, like Blue Buffalo, were expensive, and the Return on Invested Capital (ROIC) has been under pressure.

From a technical standpoint, the stock has broken through multi-year support levels. We are in extreme oversold territory on the weekly RSI. Historically, when a Blue Chip company like General Mills hits these levels of devaluation without its core business being insolvent, it is usually the prelude to a “V-shaped” recovery or, at the very least, a strong consolidation base.

Frequently Asked Questions (FAQ)

1. Why did General Mills (GIS) shares drop 3% today?

The shares fell due to a 37% drop in adjusted EPS and an 8% decline in net sales, reflecting severe margin contraction caused by heavy marketing investments and divestiture impacts.

2. Is the General Mills dividend safe in 2026?

Yes, despite the pressure on earnings, operating cash flow remains solid. The company has reaffirmed its commitment to its dividend policy, although the payout ratio margin has narrowed.

3. What is the “Remarkability Playbook” mentioned by the company?

It is General Mills’ marketing and innovation strategy designed to increase brand competitiveness by investing in advertising and product renovation to combat market share loss to private labels.

4. What is the impact of selling the Brazil business?

The sale to 3corações removes approximately $350 million in annual revenue but allows the company to focus on markets and products with higher profit margins, improving its long-term financial profile.

Conclusion: My Position and the Way Forward

Looking at everything presented, my conclusion is one of strategic caution. General Mills is not a dying company; it is a giant in metamorphosis. The sale of the Brazil business and the exit from the yogurt segment are necessary steps for a firm that had lost its way in its own complexity.

I am maintaining my position in my portfolio, as I believe in the intrinsic value of the remaining brands. However, I am not blind to market signals. The 60% drop is a red flag that the traditional business model for Consumer Packaged Goods (CPG) companies is under siege.

I am now waiting for my usual technical and fundamental signals before I look to add to my position. I want to see a stabilization of operating margins in Q4 and proof that organic sales volumes have stopped declining. If current support holds and we see a reversal in the short-term trend, GIS could be the best “recovery” play in my portfolio for the second half of 2026. Until then, patience remains the investor’s best tool.

Related posts:

My 2026 Bet on General Mills (GIS): Why Defensive Stocks Are My Sanctuary in an Overheated Market

My 2026 Bet on General Mills (GIS): Why Defensive Stocks Are My Sanctuary in an Overheated Market

General Mills (GIS) Stock Plunges 6% After 2026 Outlook Cut: Should You Buy the Dip or Walk Away?

General Mills (GIS) Stock Plunges 6% After 2026 Outlook Cut: Should You Buy the Dip or Walk Away?

The Civil War at the Federal Reserve: Is Jerome Powell’s Resistance the Last Stand for Economic Stability?

The Civil War at the Federal Reserve: Is Jerome Powell’s Resistance the Last Stand for Economic Stability?

Trade War 2.0 Greenland: How to Shield Your Portfolio Against New NATO Tariffs and Arctic Volatility

Trade War 2.0 Greenland: How to Shield Your Portfolio Against New NATO Tariffs and Arctic Volatility