Wolters Kluwer (WKL) emerges in 2026 as a rare value opportunity. Following a 67% correction from its peaks, the company trades at a P/E ratio of 12x against an expected EPS of nearly €7 in 2028. With 83% recurring revenue and an aggressive integration of Generative AI into its “Expert Solutions,” WKL balances financial resilience with tech-driven growth. The 3.55% dividend yield and consistent buybacks reinforce a thesis of superior total shareholder return.

1. The Genesis of a Giant: From 19th-Century Print to 2026 Software

To truly grasp the essence of Wolters Kluwer, one must look back at its deepest roots, which stretch to the mid-19th century in the Netherlands. The company as we know it today resulted from the 1987 merger between Wolters Samsom and Kluwer, two publishers that once dominated the professional information landscape. However, what fascinates me about this organization is not its printed past, but its absolute metamorphosis. Over the last two decades, WKL has executed one of the most successful digital transitions in European corporate history, evolving from a “publisher” into a global leader in professional information, software solutions, and services.

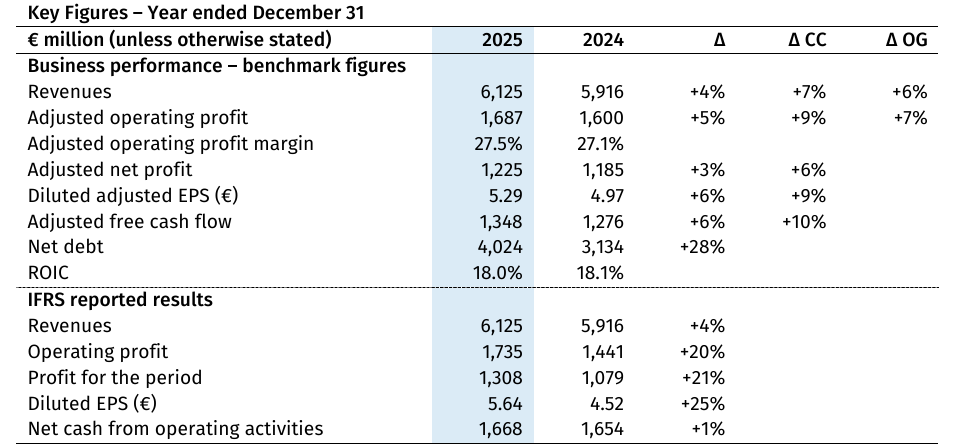

I consider Wolters Kluwer the “central nervous system” of critical sectors. If a physician needs to make an evidence-based clinical decision, they use UpToDate. If an accountant needs to ensure tax compliance in a volatile regulatory environment, they rely on WKL’s tools. This functional ubiquity creates a moat that is almost impenetrable. Today, the company operates across four main divisions: Health, Tax & Accounting, Financial & Corporate Compliance, and Legal & Regulatory. What strikes me most is the weight of recurring revenues—which reached 83% in 2025—providing a predictability of cash flows that few assets in the market can replicate. This resilience is the pillar of my confidence in holding this asset for many years to come.

2. Business Segmentation and the Power of Operational Efficiency

When analyzing the earnings structure, it becomes clear that Wolters Kluwer is not just a software company; it is an applied knowledge company. While the Tax & Accounting division remains a profitability engine, the greatest potential for accelerated growth lies within Health and Cloud Software solutions. By 2025, cloud software already accounted for 21% of total revenues, growing at organic rates of 15%. This shift to the cloud not only expands margins but also increases switching costs for the client, solidifying retention.

I view ROIC (Return on Invested Capital) as the ultimate barometer of management quality. WKL has consistently improved its ROIC, climbing from 12.3% in 2020 to an impressive 18.1% in 2024, maintaining an upward trajectory through 2025. This proves that the management team—led for years by the iconic Nancy McKinstry—knows exactly where to allocate capital to generate real shareholder value. Operational efficiency is further evidenced by the adjusted operating margin, which scaled to 27.5% at the close of 2025. For me, investing in a company that expands margins while investing heavily in innovation is the very definition of intelligent investing.

3. The AI Revolution: The Silent Catalyst

Many investors fear that AI might cannibalize professional information firms. I, on the contrary, see AI as the strongest tailwind in Wolters Kluwer’s history. The company isn’t just “using” AI; it is embedding it into the core of its Expert Solutions. By utilizing Large Language Models (LLMs) trained on its own proprietary, specialist-curated data, WKL offers something a generic ChatGPT never could: legal and medical authority and precision.

The integration of generative AI allows WKL subscribers to receive instant answers to complex queries, saving hours of manual research. This justifies price increases and enhances the value proposition. In 2026, AI is no longer a promise; it is a component driving organic growth above historical averages. The company’s ability to transform raw data into actionable decisions via proprietary algorithms is what will ensure it remains indispensable over the next decade.

4. Earnings History and the Growth Table

The financial consistency of Wolters Kluwer is, in my view, a masterpiece of financial and operational engineering. Even during periods of macroeconomic uncertainty and high interest rates set by the ECB, the company remained committed to growing its earnings per share (EPS). Below, I present a table synthesizing the robust evolution of revenue and profits, illustrating why this company is a capital “compounding machine.”

| Year | Revenue (€ Millions) | Organic Growth (%) | Adj. Diluted EPS (€) | Dividend per Share (€) |

| 2020 | 4,603 | 2% | 3.13 | 1.36 |

| 2021 | 4,771 | 6% | 3.38 | 1.57 |

| 2022 | 5,453 | 6% | 4.14 | 1.81 |

| 2023 | 5,584 | 6% | 4.55 | 2.08 |

| 2024 | 5,916 | 6% | 4.97 | 2.33 |

| 2025 | 6,125 | 6% | 5.29 | 2.52 |

| 2026 (Est.) | ~6,500 | ~7% | ~6.95 | ~2.80 |

Source: Internal analysis based on Wolters Kluwer Annual Result Reports (2020-2025).

As we can observe, the progression is linear and relentless. The EPS has nearly doubled in six years, driven by a combination of organic growth, margin expansion, and an aggressive share buyback policy. Between 2022 and 2025 alone, the company executed billions of euros in buybacks, reducing the share count and increasing the slice of profits for each remaining shareholder.

5. Why I Initiated a Position at €68: From Overpriced to “Steal”

Financial markets are often irrational. Wolters Kluwer once traded at multiples I considered unsustainable, fueled by tech euphoria. However, the recent technical “crash” and asset rotation caused the stock price to drop more than 67% from its all-time highs. A company with these fundamentals dropping 67% is a signal I simply could not ignore. I initiated my position this week around €68.

At this price level, we are looking at a P/E (Price-to-Earnings Ratio) of just 12x based on expected 2026 earnings (estimated at nearly €7 per sharein 2028). For a software-heavy company with 83% recurring revenue and 27% margins, a 12x P/E is, in my technical opinion, a market anomaly—it is “dirt cheap.” Furthermore, the current 3.55% Dividend Yield provides an additional safety net and growing passive income, given the company’s history of double-digit dividend hikes.

6. Technical Analysis: The Heikin Ashi Filter

While my analysis is predominantly fundamental, I use technical timing to optimize my entries. In my February 2026 portfolio close, I highlighted the importance of following medium-term trends. For WKL, my rule is clear: I will continue to add to the position as long as the Heikin Ashi candles remain green on the weekly chart.

Heikin Ashi candles filter out market noise and reveal the true strength of a trend. After the brutal drop from the highs, we are finally seeing a reversal in the price structure. If the weekly momentum stays positive, I will apply the Dollar Cost Averaging (DCA) technique to build a long-term core position. The goal isn’t to time the exact “bottom,” but to accumulate an extreme-quality asset while the market is still in shock.

7. Challenges and Opportunities on the 2026 Horizon

No investment is without risk, and as a senior finance writer, it is my duty to point out the hurdles.

- Currency Risk: With significant exposure to the US market, fluctuations between the Euro and the Dollar can impact reported results.

- AI Execution: While AI is an opportunity, technical execution and data privacy are critical. Any failure in the accuracy of Health or Legal solutions could damage brand reputation.

- Macro Scenario: A deep recession in Europe could slow down non-recurring sales and new subscriptions, though the recurring base acts as a massive buffer.

However, the opportunities far outweigh the risks. The consolidation of new markets, the full migration of clients to SaaS solutions, and the potential use of a strong balance sheet (Net-debt-to-EBITDA of 2.0x) for strategic acquisitions are potent catalysts. WKL is a classic “compounder” that benefits from global regulatory complexity: the more laws and norms exist, the more businesses need Wolters Kluwer.

8. FAQ: Frequently Asked Questions about Wolters Kluwer (WKL)

Is Wolters Kluwer a good dividend investment?

Yes. With a 3.55% Dividend Yield in 2026 and a history of annual dividend growth exceeding 10%, it is a solid choice for income-focused investors looking for growth.

What is the impact of Artificial Intelligence on WKL?

AI is a growth catalyst. The company uses generative AI to make its expert solutions faster and more precise, allowing it to maintain its strong pricing power.

Why did the stock drop 67% if fundamentals are good?

The drop was primarily due to a correction of overstretched valuation multiples combined with a macroeconomic rotation. The underlying business remains robust, making the current price a significant valuation opportunity.

Conclusion: A High-Conviction Thesis for the Next Decade

In summary, my thesis on Wolters Kluwer is built on the perfect convergence of fundamental quality and attractive pricing. We aren’t buying a speculative promise, but a market leader with over a century of history that successfully reinvented itself for the digital age and now for the AI era. The current valuation of 12x earnings is, in my view, a gift from the market to those with long-term vision.

I will hold this position in my portfolio with the conviction that time is the best friend of extraordinary companies traded at ordinary prices. I will closely monitor the weekly Heikin Ashi candles and will not hesitate to increase my exposure. For further details on official results, please refer to the Wolters Kluwer Investor Relations page.

Disclaimer: This article reflects my personal opinion and does not constitute personalized financial advice. Investing in stocks involves risk and should be done based on your own analysis or by consulting a certified professional.

Related posts:

Ferrari Stock: Why I’m Buying Ultra-Luxury at a 40% Discount?

Ferrari Stock: Why I’m Buying Ultra-Luxury at a 40% Discount?

Skin in the Game: Portfolio January 2026 – Why I Doubled Down on Constellation Software (CSU)

Skin in the Game: Portfolio January 2026 – Why I Doubled Down on Constellation Software (CSU)

S&P Global’s 10% Dip: Generative AI Threat or a Generational Buying Opportunity?

S&P Global’s 10% Dip: Generative AI Threat or a Generational Buying Opportunity?

The 2026 Portfolio State of Play: Why My “Resilient Growth” Strategy Is Ignoring the Market Noise

The 2026 Portfolio State of Play: Why My “Resilient Growth” Strategy Is Ignoring the Market Noise