Palantir Technologies (PLTR) remains a cornerstone of the 2026 AI economy, boasting 70% Y/Y revenue growth and an unprecedented 127% Rule of 40 score. Despite its strategic dominance in U.S. Defense and a 137% surge in U.S. Commercial revenue, its 229x P/E ratio signals extreme overvaluation. My thesis suggests capital patience: waiting for the $75–$98 support zone to capture a projected $6.00 EPS by 2029, offering superior long-term risk-adjusted returns.

My Palantir investment thesis for 2026 is built on a single, unwavering principle: I invest in foundational monopolies, but I never overpay for them. As we stand here in March 2026, Palantir Technologies Inc. has successfully transitioned from a controversial “black box” of Silicon Valley into the literal central nervous system of Western institutional power. However, as an investor focused on the margin of safety, I cannot ignore the technical overextension on the charts. I am personally waiting for Palantir to retraced into the green shaded zone, and in this deep dive, I will explain why this is the only rational move for those looking to build generational wealth through 2029. February 2026 Portfolio Close

1. What is Palantir? A Deep Dive for the Uninitiated

If you are new to the story, you might think of Palantir as just another “AI company.” That is a fundamental misunderstanding. Most AI companies today focus on generative tasks—writing emails or creating images. Palantir focuses on operational decision-making. I often describe Palantir as a “Digital Operating System” for the modern enterprise. They don’t just provide a tool; they provide an Ontology—a digital twin of an entire organization where every sensor, every spreadsheet, and every satellite feed is integrated into a single, cohesive truth.

The company’s architecture is divided into four pillars that constitute its massive competitive advantage:

- Gotham: The platform for government and defense. It allows agencies to identify needles in haystacks, from uncovering human trafficking rings to planning complex military maneuvers in active war zones.

- Foundry: The commercial equivalent. Large-scale enterprises like BP or Airbus use Foundry to manage global supply chains, reducing costs by billions through real-time data orchestration.

- Apollo: The continuous delivery software that ensures these platforms can run anywhere—on a cloud server, in a submarine, or on a drone at the edge of the battlefield.

- AIP (Artificial Intelligence Platform): The 2026 growth engine. AIP allows companies to deploy Large Language Models (LLMs) safely within their private networks, turning raw data into actionable intelligence without compromising security.

2. Geopolitics, Sovereignty, and the “War” Advantage

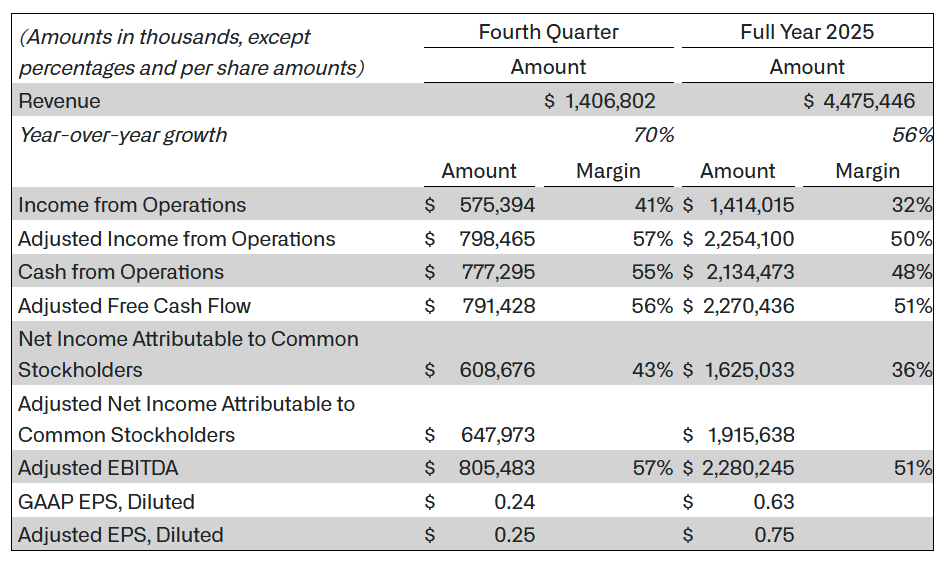

We cannot analyze Palantir without discussing sovereignty. In 2026, data is the new oil, and processing speed is the new ammunition. Palantir has positioned itself as the indispensable partner for the U.S. Department of Defense and its allies. According to the latest earnings report from February 2, 2026, U.S. Government revenue grew by a staggering 66% year-over-year, reaching $570 million in Q4 alone.

I view Palantir as a “Defense Prime” disguised as a SaaS company. In an era of global instability, the ability to achieve “commodity cognition”—a term coined by CEO Alex Karp to describe the rapid scaling of operational leverage—is what wins conflicts. This creates an unshakeable Moat. Once a government integrates its intelligence apparatus into Gotham, the switching costs are virtually infinite. However, this is a double-edged sword. The heavy reliance on government contracts remains a key risk, although the 137% growth in U.S. Commercial revenue proves they are rapidly diversifying their income streams.

Comparative Data: Performance vs. Projections

| Metric | Q4 2025 Actuals | FY 2026 Guidance | Strategic Insight |

| Total Revenue | $1.407 Billion | +61% Y/Y | Hyper-growth sustained |

| U.S. Commercial Rev | $507 Million | +115% Y/Y | Massive market capture |

| Rule of 40 Score | 127% | >100% (Est.) | Best-in-class efficiency |

| Gross Margin | 82.37% | Stable | High pricing power |

| ROIC | 21.46% | Rising | Efficient capital recycling |

3. Technical Analysis: Why the “Green Zone” Matters

Looking at the current daily chart (March 2, 2026), PLTR is trading around $145.17. While the business fundamentals are flawless, the valuation is decoupled from reality. We are looking at a P/E ratio of 229.41 and an Enterprise Value/Sales of 76.05x. For even the most aggressive growth investor, these numbers are “priced for a perfection” that rarely exists in volatile markets.

Calculating the Value in the Support Zone

My target for entry is the green shaded area between $75 and $98. This zone aligns with historical support and the long-term weighted moving average (WMA). If the stock corrects to a median price of $85: Adjusted P/E approx 135x.

While 135x still sounds expensive, when we factor in the forward-looking EPS estimates of $1.30 to $1.85 for late 2026, an $85 entry price brings the Forward P/E down to a much more palatable 46x–65x. For a company growing its top line at 61%–70%, this is the “Goldilocks zone” where risk and reward finally balance out.

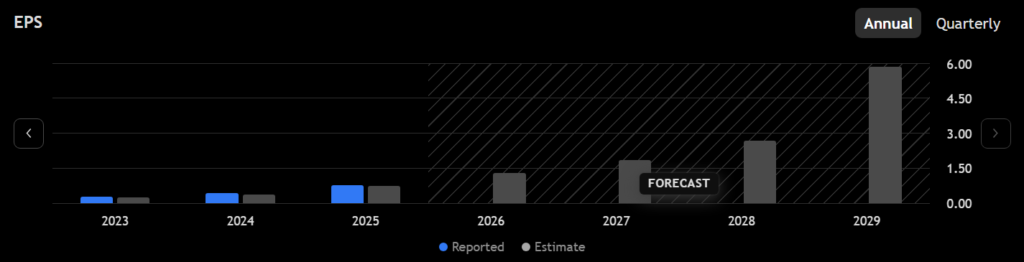

4. The Path to 2029: Projected Profitability

The core of my long-term bull case lies in the exponential earnings growth forecasted over the next three years. Analyst estimates suggest a leap to an EPS of $6.00 by 2029. This reflects the full-scale maturation of AIP and the widespread adoption of Palantir’s “Bootcamp” sales model, which has drastically reduced the customer acquisition cycle.

Projected Returns (Buying at $85 Target -> 2029 Exit):

- Conservative Scenario: If PLTR hits $6.00 EPS and the market assigns a mature software multiple of 30x.

- Price Target = 6.00 x 30 = $180.00.

- Total Return: approx 112%.

- Bullish Scenario: If the market maintains a 50x multiple due to Palantir’s monopoly on “AI Sovereignty.”

- Price Target = 6.00 x 50 = $300.00.

- Total Return: approx 253%.

Buying today at $145 significantly dilutes this upside and leaves you vulnerable to a 35%–45% drawdown if the market experiences a general “AI fatigue” correction. I prefer to let the price come to me.

5. Moat, ROIC, and the Efficiency Fortress

I am particularly impressed by the ROIC (Return on Invested Capital) of 21.46%. This tells me that Alex Karp’s management team is expertly deploying capital to generate high-quality profits. Furthermore, with a Debt/Equity ratio of only 0.03, Palantir is essentially a debt-free fortress.

Their Moat is built on three pillars:

- Sticky Revenue: Palantir doesn’t just sell software; it embeds itself into the client’s culture. Removing Foundry from a company like Airbus would be like trying to perform a heart transplant while the patient is running a marathon.

- Data Dominance: As more data flows through their ontologies, the models become more accurate, creating a powerful Network Effect for existing users.

- High Switching Costs: The training and integration required to use Palantir create a natural barrier against competitors.

6. Risks and Competitors

No investment is without peril. I am closely monitoring the following:

- Customer Concentration: Despite the commercial explosion, the loss of a major U.S. Army contract would cause a significant, albeit perhaps temporary, collapse in sentiment.

- Competition: We are seeing increased pressure from Snowflake (in data warehousing), C3.ai (in niche enterprise apps), and the “Hyperscalers” like Microsoft Azure and AWS, who are trying to build their own end-to-end AI stacks. However, Palantir’s “un-opinionated” approach to data allows it to sit on top of these clouds, which remains its greatest tactical advantage.

- Valuation Risk: In 2026, the biggest risk isn’t the company failing; it’s the investor overpaying. A 229x P/E requires flawless execution.

FAQ – Investor Frequently Asked Questions

Is Palantir a “Defense” or “Tech” stock?

It is both. In 2026, the distinction is blurring. Palantir provides the software that powers modern defense, making it a “Software Defense Prime.”

Why should I wait for the $75–$98 range?

Historically, high-growth stocks like PLTR undergo “mean reversion.” Buying at $145 exposes you to a high probability of “buying the top” before a healthy market correction.

What is the significance of the “Rule of 40” score?

A score of 127% is legendary. It means the sum of their growth rate and profit margin is far above the 40% benchmark used to identify elite SaaS companies.

Conclusion: The Final Verdict

Ultimately, Palantir is an extraordinary company at an ordinary (and expensive) price. My investment thesis is simple: Do not chase the candle. The business is firing on all cylinders, with 36% profit margins and growth that continues to “crush consensus expectations”.

Waiting for the green zone ($75–$98) is not just a technical preference; it is a discipline. It ensures that when 2029 arrives and we see that $6.00 EPS, our returns are not just “market-beating” but life-changing. If the stock never drops to that level, I am content to stay on the sidelines. But if it hits that zone, I will be ready to deploy capital aggressively into the company that I believe will define the next decade of institutional intelligence.

Disclaimer: This article represents my personal opinion and fundamental/technical analysis. It does not constitute financial advice. Investing in the stock market involves high risk and the potential for total loss of capital. Perform your own due diligence.

Related posts:

Silver in 2026: Is This Price Explosion Just the Beginning or a Short-Term Trap?

Silver in 2026: Is This Price Explosion Just the Beginning or a Short-Term Trap?

Bitcoin DCA Strategy with Heikin Ashi: My Blueprint to Defeat Fiat Currency Devaluation

Bitcoin DCA Strategy with Heikin Ashi: My Blueprint to Defeat Fiat Currency Devaluation

Is the Stop Loss Obsolete? Why in 2026 I Use Hedging as My Antifragile Shield

Is the Stop Loss Obsolete? Why in 2026 I Use Hedging as My Antifragile Shield

The Death of the Stop Loss? My Forex Trading Strategy Based on Cyclicality and Proportional Volume

The Death of the Stop Loss? My Forex Trading Strategy Based on Cyclicality and Proportional Volume