As of February 2026, my portfolio state of play centers on a strategic pivot toward long-term fixed income (41.3% in US Treasuries) and high-quality technology (MSFT). Diversified across defensive sectors (GIS) and luxury (RACE), the portfolio prioritizes “moat-heavy” firms with sustainable EPS growth. I am currently capitalizing on the software sector correction and the divergence between real-time inflation data (Truflation) and lagging official BLS reports to accumulate undervalued assets.

1. The Long-Term Philosophy: Looking Beyond the “100-Bagger” Mirage

Many investors spend their entire careers chasing the “next big thing”—that elusive penny stock or speculative tech play that promises to multiply their capital a hundredfold overnight. I am not that investor. The portfolio state of play I am presenting to you today is the result of rigorous discipline focused on capital preservation and compound growth. My goal is to build a long-term portfolio composed of companies that don’t need miracles to thrive, but rather solid operational execution and a clear economic moat.

As I detail in my guide on how to pick stocks to buy, I focus on stable companies with consistent Earnings Per Share (EPS) growth and business models that can withstand adverse economic cycles. In 2026, with the market showing sharp volatility after years of AI-driven euphoria, this “balanced sectors” approach has been my anchor.

I firmly believe that the future is technological, which justifies my bias toward large-cap software and semiconductor firms. However, balance is the master key. You don’t build a castle out of glass alone; you need stone and mortar. This is why, alongside Microsoft, I maintain significant positions in staples like General Mills (GIS). In a scenario where the cost of living still pressures households, holding a company that yields over 5% in dividends in a defensive sector is, in my view, a matter of financial sanity.

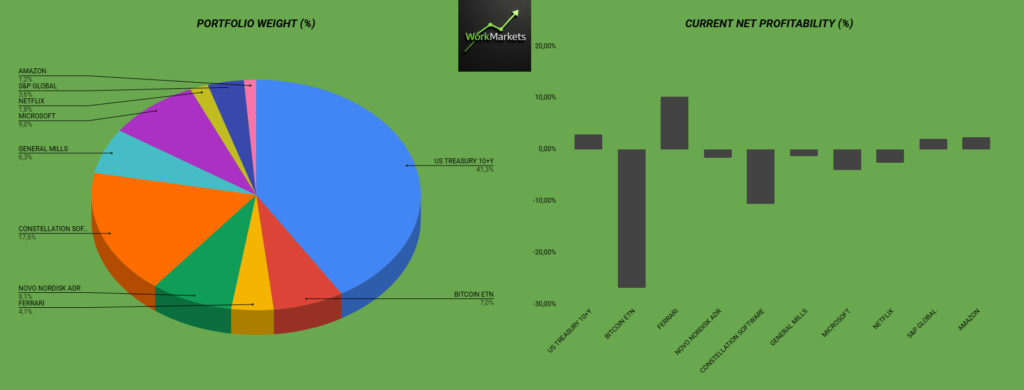

2. Portfolio Radiography: Weights and Allocations in 2026

To analyze performance, we must look at the cold, hard numbers. The portfolio state of play reveals a tactical concentration in assets that offer protection against the GDP slowdown we’ve begun to see in recent reports from the Bureau of Economic Analysis (BEA).

Table: Portfolio Composition and Current Performance

| Asset | Portfolio Weight (%) | Current Net Profitability (%) | Investment Thesis |

| US Treasury 10+Y (TLT) | 41.3% | +3.0% | Bet on falling interest rates and macro protection. |

| Constellation Software (CSU) | 17.6% | -11.0% | Vertical Market Software (VMS) compounder in correction. |

| Microsoft (MSFT) | 9.0% | -4.0% | AI leader with attractive valuation metrics. |

| Novo Nordisk ADR (NVO) | 8.1% | -1.5% | Dominance in the GLP-1 (obesity/diabetes) market. |

| Bitcoin ETN | 7.0% | -27.0% | High-risk asset and digital store of value (correcting). |

| General Mills (GIS) | 6.3% | -1.0% | Stable dividends and defensive consumption. |

| Ferrari (RACE) | 4.1% | +10.0% | Absolute luxury with unbeatable pricing power. |

As you can see, my largest position is not a stock, but US Government Debt. This decision isn’t born of fear, but of mathematical opportunity.

3. The “Software Winter” and the Magnificent 7 Correction

We are living through a peculiar moment in 2026. The software sector, the darling of the last decade, is being severely punished. The most glaring example in my portfolio is Constellation Software (CSU). Seeing a company of this quality drop more than 50% from its all-time highs is enough to make many investors panic. I, on the other hand, see this as a necessary cleansing.

The so-called Magnificent 7 (Microsoft, Apple, Nvidia, etc.) are also undergoing a correction this year. The market is finally demanding proof that the massive AI investments are translating into even higher profit margins. This drawdown has created “value zones” in companies that were previously inaccessible due to their stratospheric multiples.

“Market volatility is the price we pay for long-term outperformance. If you can’t stomach a 50% drop in a great company, you don’t deserve the returns it will generate over the next decade.”

4. A Generational Opportunity: Why Microsoft (MSFT) Is My Priority

If you were to ask me what the most evident opportunity in the portfolio state of play is, the answer is immediate: Microsoft.

When we analyze the XLP/MSFT ratio (Consumer Staples vs. Microsoft), we notice something fascinating. Microsoft is trading at levels that historically represent fundamental psychological and technical support points. Currently, the company presents a Forward P/E (Price-to-Earnings) of 22. For an entity that dominates the cloud infrastructure with Azure and has integrated AI across its entire productivity ecosystem, this multiple is, in my opinion, a gift.

I intend to continue doubling down on MSFT aggressively. We aren’t talking about a speculative tech firm, but a free-cash-flow generating machine. When the market recovers from its current “sentiment hangover,” companies with growing EPS and bulletproof balance sheets will be the first to lead the charge.

5. The Treasury Thesis: The End of Inflation and the BLS Error

The second major opportunity, and the reason I hold 41.3% in US Treasury 10+Y, is rooted in macroeconomics. As I discussed in my article on the end of inflation, I believe the Federal Reserve (Fed) is on the verge of a significant rate-cutting cycle.

Why am I so assertive about this? Because Bureau of Labor Statistics (BLS) data is notoriously lagging. While official reports still show resilient inflation, real-time indicators like Truflation already demonstrate deflation across various sectors of the economy. Furthermore, the lower GDP figures recently reported suggest the US economy is cooling faster than expected.

Technically, the TLT (iShares 20+ Year Treasury Bond ETF) chart shows a massive surge in volume. This indicates institutional accumulation. While the Fed hasn’t officially pulled the trigger on cuts yet, I am happy to “sit” on the position and collect a yield of over 4%, which is extremely attractive in a low-growth environment.

6. New Horizons: Analyzing Sprouts Farmers Market (SFM)

In addition to reinforcing existing positions, I am always hunting for new names that fit my “moat and growth” philosophy. Currently, my lens is focused on Sprouts Farmers Market (SFM).

What attracts me to SFM?

- Market Niche: A total focus on organic and healthy products—a sector that continues to grow despite inflationary pressures.

- Quality Metrics: The company boasts an enviable ROIC (Return on Invested Capital) and very disciplined capital management.

- Pricing: Much like the rest of the market, SFM has seen significant pullbacks from its highs, allowing me to enter a high-quality business with a significant margin of safety.

FAQ: Frequently Asked Questions on the Portfolio State

1. Why hold Bitcoin if the position is down over 25%?

The Bitcoin ETN is my “call option” on the global financial system. The 7% weight is controlled; volatility is expected and does not change the thesis of digital scarcity in the long run.

2. Is it worth investing in Treasuries when US debt is so high?

Yes, because in the short-to-medium term, the direction of interest rates dictates the price of the bonds. Real-time falling inflation will force the Fed to act to prevent a deep recession, driving bond prices up.

3. Isn’t General Mills (GIS) too “slow” for a tech-heavy portfolio?

GIS isn’t there to be fast; it’s there to be safe. Its 5% dividend funds my patience while I wait for the growth theses (like MSFT and CSU) to play out.

Conclusion: Discipline Over Euphoria

The portfolio state of play in 2026 reflects a position of cautious optimism. I am not trying to time the absolute bottom, but I am buying value where it is undeniable. The combination of Microsoft at a reasonable price with the protection and income of Treasuries puts me in a position of strategic advantage.

My next moves are clear: add to MSFT and TLT as long as market conditions persist. I will continue to build smaller positions gradually, always keeping the focus on EPS growth and business resilience. At the end of the day, investing isn’t about being right every week—it’s about being positioned correctly for the next ten years.

Disclaimer: This article represents my personal opinion and the strategy used in my own portfolio. It does not constitute financial advice. Only invest capital you are comfortable losing and conduct your own due diligence.

Related posts:

Constellation Software (CSU): Why I Am Aggressively Doubling Down on This Generational Opportunity Amidst Extreme Market Fear

Constellation Software (CSU): Why I Am Aggressively Doubling Down on This Generational Opportunity Amidst Extreme Market Fear

Why Constellation Software is My Only Choice: The Death of Horizontal Software and the Resilience of VMS

Why Constellation Software is My Only Choice: The Death of Horizontal Software and the Resilience of VMS

Skin in the Game: Portfolio January 2026 – Why I Doubled Down on Constellation Software (CSU)

Skin in the Game: Portfolio January 2026 – Why I Doubled Down on Constellation Software (CSU)

TLT Opportunity 2026: Why I’m Betting Big on US Treasuries and the Dollar

TLT Opportunity 2026: Why I’m Betting Big on US Treasuries and the Dollar