As of January 2026, Constellation Software (CSU) is experiencing a historic 40% drawdown, driven by market fears that Generative AI will disrupt Vertical Market Software (VMS). However, CSU’s fundamentals remain record-breaking, with a Forward PER of 19x and Price-to-FCF of 18x—valuation levels not seen since 2014. With the weekly RSI at extreme oversold levels, the bull case rests on the “moat” of domain expertise and AI-driven operational efficiencies.

I have always maintained that successful investing is less about raw intelligence and more about temperament. Today, January 15, 2026, I find myself in a position that many would deem uncomfortable, yet for me, it is the natural “habitat” of a value-oriented investor: I am aggressively buying shares of Constellation Software (CSU) while panic permeates the market. Constellation Software is, and continues to be, the backbone of my long-term investment strategy, holding a prestigious spot alongside titans like Novo Nordisk (NVO) and General Mills (GIS) in my personal portfolio.

The current narrative is undeniably grim. If you open any financial terminal or listen to “momentum” analysts, the tune is the same: Artificial Intelligence will decimate vertical software; clients will build their own solutions using LLMs; Mark Leonard’s empire has reached its expiration date.

I profoundly disagree. What we are witnessing is not the death of a business model, but rather one of the most significant dislocations between price and intrinsic value I have seen in the last decade. With shares trading around 3,165 CAD after retreating from the 5,000 CAD mark, the market is handing us a blue-chip asset at a fire-sale price. In this article, I will detail why my optimism regarding CSU is unshakable, analyzing everything from the company’s genesis to the rare technical opportunity the RSI presents at this moment.

1. The Architect of the Machine: Mark Leonard and the VMS Empire

To understand why Constellation Software is a unique asset, one must look back at the figure of Mark Leonard. Often referred to as “The Canadian Warren Buffett,” Leonard founded CSU in 1995 with a simple yet revolutionary premise: acquire Vertical Market Software (VMS) companies that dominate specific niches and generate highly predictable cash flows.

I consider Mark Leonard to be one of the greatest capital allocators in history. His philosophy is not built on speculative “hyper-growth” but on operational efficiency and customer retention. The business model of CSU is what we call a “serial acquirer” or a “roll-up,” but with a twist of extreme discipline. They purchase small software firms that solve mission-critical problems for very specific industries—ranging from library management to billing systems for maritime shipping. This software is often the “glue” that keeps these businesses running; the cost of switching to a competitor is immense (high switching costs), which grants CSU phenomenal pricing power and retention rates that border on perfection.

The history of CSU is a lesson in discipline. Leonard has famously never overpaid for acquisitions, consistently maintaining return on invested capital (ROIC) metrics far above the industry average. Over the years, the company has decentralized, creating six autonomous operating groups (Varis, Harris, Jonas, Vela, Perseus, and Topicicus) that allow Constellation to scale even as a multi-billion dollar giant. Investing in CSU is, in my view, investing in a culture of excellence that transcends any single individual.

2. The Great AI Fear: Narrative vs. Operational Reality

Why has Constellation Software plummeted so significantly throughout 2025 and into early 2026? The short answer is: AI Uncertainty. The market fears that Large Language Models (LLMs) will allow CSU’s clients to build their own niche software “at the push of a button,” or that “AI-native” competitors will emerge from nowhere to seize market share.

However, my analysis indicates the exact opposite. CSU’s VMS is not just lines of code; it is accumulated domain knowledge spanning decades. An LLM can write code, but it does not understand the tax intricacies of waste management in Ontario or the specific regulatory hurdles of a hospital in Germany. AI is a tool that CSU is already utilizing to lower its own development and maintenance costs.

I view AI as a silent ally. Contrary to market consensus, Constellation is in a privileged position to integrate AI into its existing products, increasing value for the client and, consequently, increasing subscription fees. We are seeing a repetition of what happened with Adobe (ADBE) and Intuit (INTU) in previous cycles: the price drops due to disruption fears, while earnings and revenues continue to hit records. As I noted, CSU is currently at all-time highs in revenue and EBITDA, making this price collapse a mathematical absurdity.

3. Fundamental Analysis: The Numbers Wall Street is Ignoring

When we examine the fundamentals, the distortion is glaring. Constellation Software is trading at multiples we haven’t seen in over ten years.

- Valuation: The adjusted Forward P/E has dropped below 20x (currently around 19x). Historically, CSU has rarely traded below 25-30x during the last decade of expansion.

- Cash Flow: The Price-to-Free Cash Flow ratio stands at 18x. For a company that compounds its FCF at double-digit rates, this is a flagrant signal of undervaluation.

- Debt and Balance Sheet: Capital management remains exemplary. CSU uses debt intelligently to fund acquisitions, but the Net Debt/EBITDA ratio remains at comfortable levels, ensuring the company can continue to buy cheap assets in this down market.

- Earnings Per Share (EPS): EPS growth estimates for 2026 and 2027 remain robust, as the company benefits from the integration of massive acquisitions made in late 2024.

Below, I present a comparative table illustrating CSU’s current attractiveness compared to its recent historical averages.

Comparative Table: Constellation Software (Valuation Metrics)

| Metric | Historical Avg (2020-2024) | Current (Jan 2026) | Variance |

| Price-to-Earnings (Forward) | 32x | 19x | -40.6% |

| Price-to-Free Cash Flow | 28x | 18x | -35.7% |

| Weekly RSI | 55 (Neutral) | 22 (Extreme) | -60% |

| EBITDA Margin | 24% | 26% | +8.3% |

| Est. EPS Growth | 15% | 18% | +20% |

Data based on official filings and market consensus for the 2026 scenario.

4. Technical Analysis: The Weekly RSI’s “Scream to Buy”

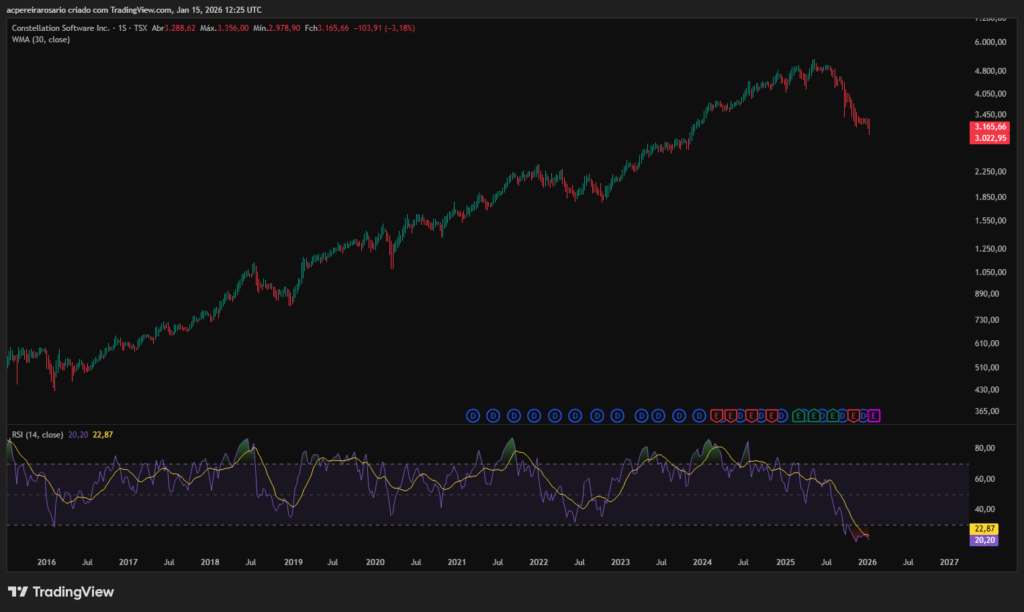

Beyond the fundamentals, the technical side of this investment is what gives me the conviction to increase my position now. If we look at the weekly chart for CSU.TO (Toronto Stock Exchange), we see an incredibly rare setup.

The Weekly RSI (Relative Strength Index) is touching oversold levels that we only see during extreme systemic crises. Trading with an RSI below 30 on the weekly timeframe, for a company of Constellation’s caliber, is almost like a “glitch in the matrix.” Historically, every time CSU has reached these levels of technical pessimism, it has been followed by a violent recovery over the subsequent 12 to 24 months.

I do not try to catch the exact bottom, but when I see a capitulation of this magnitude, my instinct is to be a buyer. The 3,165 CAD price point represents a fundamental psychological and technical support level. We are looking at a drawdown of over 40%, surpassing the 2022 correction and approaching the severity of 2008 in terms of sentiment. My stance is clear: I am utilizing current liquidity to increase my portfolio weight.

5. My 2026 Portfolio Strategy: CSU, NVO, and GIS

Despite the volatility in Constellation, my overall investment portfolio has shown remarkable resilience. Currently, my Year-to-Date (YTD) 2026 portfolio return is hovering around 8%, a result I consider excellent given the turbulence in the tech sector.

This performance is sustained by a strategic “barbell” diversification:

- Novo Nordisk (NVO): The pharmaceutical giant remains a growth engine, benefiting from the unrelenting demand for metabolic treatments and its dominance in the GLP-1 space.

- General Mills (GIS): My conservative bet in the consumer staples sector. As I detailed in my previous analysis, My 2026 Bet on General Mills, GIS provides the dividend stability and defensive margins that balance CSU’s temporary aggression.

Having Constellation at these prices while NVO and GIS anchor the portfolio’s value allows me to sleep soundly. I view CSU as a “growth compounder” with a “distressed asset” discount—a delicious risk-reward asymmetry.

Frequently Asked Questions (FAQ)

1. Why did Constellation Software (CSU) stock drop so much in 2026?

The decline is primarily driven by investor fear that Generative AI will commoditize niche vertical software and a broader rotation away from software multiples, leading to a de-rating from 30x to 19x Forward P/E.

2. Is Mark Leonard still involved in the management?

Yes. While Mark Leonard has delegated many day-to-day operations to the presidents of the six operating groups, his rigorous capital allocation culture and long-term vision remain the bedrock of the company’s competitive advantage.

3. Does Constellation Software pay a dividend?

CSU pays a nominal dividend, but the company’s primary focus is the total reinvestment of free cash flow into new acquisitions, creating a compounding effect for long-term shareholders.

4. Is it worth buying CSU now with such a low RSI?

Technically, a weekly RSI below 25 is a historic “buy” signal for high-quality compounders. For long-term investors who trust the fundamentals, this level has historically represented an optimal entry or reinforcement point.

Conclusion: Value Always Prevails Over Noise

In summary, my conviction in Constellation Software (CSU) has never been stronger. We are facing a company that dominates its market, led by a culture of excellence, which is currently being sold at “bargain-basement” prices by an emotionally unstable market.

I do not fear Artificial Intelligence; I fear not having enough capital to buy every share I want at these levels. CSU is a cash-generating machine that adapts, survives, and thrives in chaos. While the majority flees, I am doubling down. By the end of 2026 or 2027, when the market realizes that VMS software is far more resilient than a chatbot, 3,165 CAD will seem like a distant memory of a missed opportunity for many.

My portfolio remains steady with an 8% YTD gain, and I am confident that Constellation will be the primary driver of our future alpha. The financial market is the only place where customers run away when high-quality products go on sale. I, for one, prefer to stay and fill the cart.

Disclaimer: This article reflects my personal opinion and investment strategy. It does not constitute financial advice. Investing in equities involves risk.

References:

- Investor Relations | Constellation Software

- Constellation Software Inc. Quarterly Reports (SEDAR)

- Mark Leonard’s Annual President’s Letters

- Market Report: “The Resilience of VMS in the AI Era” – Global Tech Analytics 2026

- Market Data via TSX and Bloomberg Terminal.